According to UnitedHealthcare’s 2017 Consumer Sentiment Survey, very few people have a full understanding of the basic health insurance concepts.

They found that only 9% of the U.S. population showed an understanding of all four of the following basic insurance terms: health plan premium, health plan deductible, out-of-pocket maximum, and co-insurance. And, that’s only a small increase from 7% in 2016.

In addition, the survey found that people had a better grasp of one or two of those terms. 61% knew what a health plan premium was, 62% recognized the definition for health plan deductible, 39% knew what an out-of-pocket maximum was and 31% had a decent understanding of co-insurance.

More people seemed to show a better understanding of an in-network provider (62%) and a co-pay (69%). Furthermore, a quite a few people were confused about the financial impact of visiting an out-of-network provider versus an in-network provider. For example, 36% of people incorrectly stated that an in-network provider would increase their bill.

I don’t know about you, but these statistics shocked me!

I would have thought more people understood the basics of how health insurance works given how much money we all spend for coverage and treatment. Not to mention the huge financial risk if we visit an out-of-network provider.

As a result, I felt obligated to write this post with the goal to help educate as many people as possible on how insurance works.

So, to get started, let’s get back to the basics with the most common health insurance definitions.

Learn the basic health insurance terms

- Health Insurance: Coverage protecting the insured (i.e. patient) from risk of significant financial loss due to health related causes (i.e. illness or injury).

- Health Plan Premium: The amount of money you pay for health insurance coverage each month. Note: you have to pay the premiums even if you never visit a doctor.

- Health Plan Deductible: The amount of money you pay out-of-pocket for health care services before your insurance coverage starts to pay anything. Note: In most cases, copays do not count toward your deductible. You should check if your plan applies copays towards your deductible or not.

- Co-Insurance: The percentage of costs of a covered health care service you must pay after you’ve paid your deductible. Note: There is typically a lower co-insurance amount (i.e. 20%) when you see a provider who is in-network compared to the amount you would pay (i.e. 40%) when visiting an out-of-network provider.

- Copayment (or Copay): A fixed amount (i.e. $25) you pay for a covered health care service, usually when you receive the service. The amount can vary by the type of covered health care service.

- Out-of-pocket Maximum (OOPM): The most you have to pay for covered health care services in a plan year. After you spend this amount, your health insurance pays 100% of the additional costs of covered benefits. Note: The out-of-pocket limit includes your deductible, co-insurance and copayment amounts. It does not include your premiums or anything you spend on services not covered by your insurance plan.

- In-network Providers: Doctors, other health care providers, and hospitals that a health insurance plan has contracted with to provide medical care to its members (i.e. you) at agreed to prices. Note: Receiving health care services at an in-network provider typically decreases your medical bill.

- Out-of-network Providers: A provider that has not contracted with the health insurance plan. Note: Receiving health care services at an out-of-network provider typically increases your medical bill.

Congratulations! Now you know more than 90% of the U.S. population when it comes to understanding these basic health insurance terms.

A patient’s journey using health insurance

Knowing the definitions is good, but understanding the health insurance concepts and how they work is even better. And, I want to make sure you have a very clear understanding of how health insurance works.

In order to do that, let’s follow a patient’s journey.

Just a heads up, the following section is essentially the same as the above infographic. Jump to the ROI section if you want to skip the patient journey narrative.

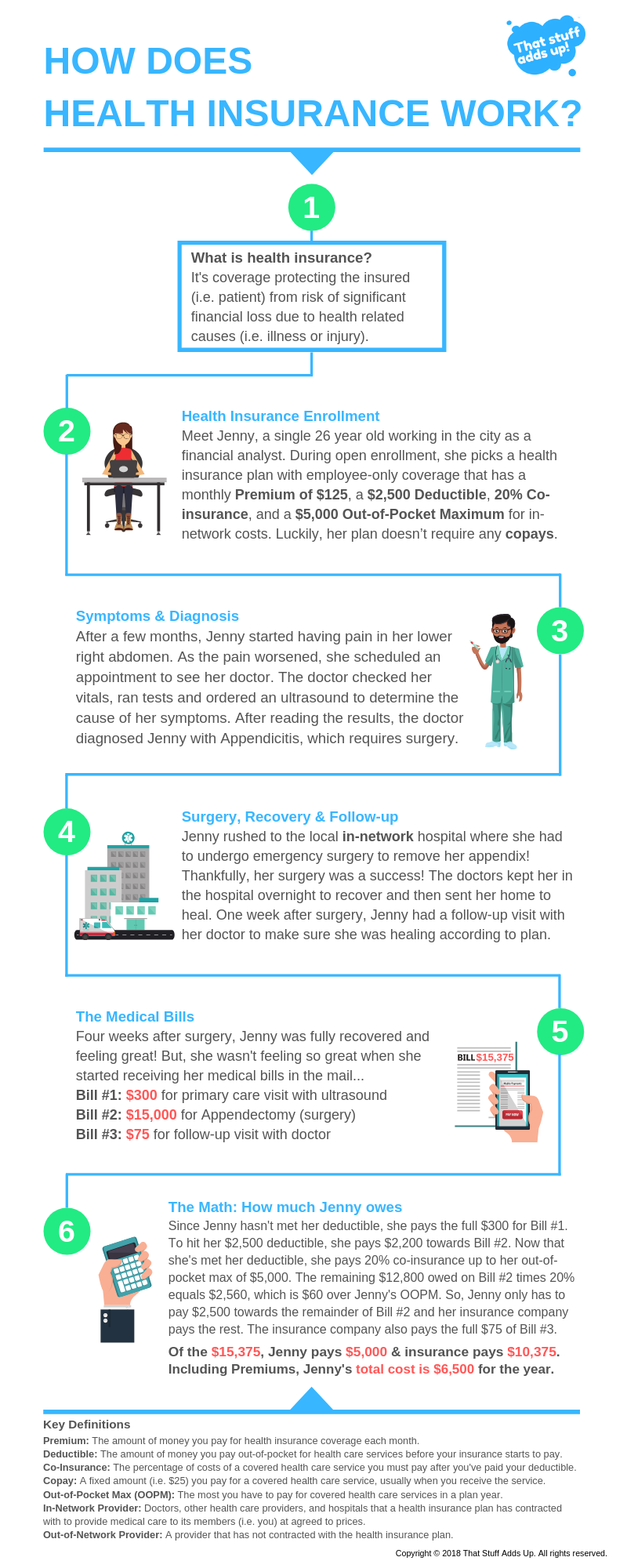

Meet Jenny, a 26 year old financial analyst who enrolled in her employer-sponsored health insurance plan. Jenny is not married and doesn’t have any dependents so she only needs insurance coverage for herself.

The Health Insurance Plan

After researching her options, she elects a health plan with employee-only coverage that has a $125 monthly Premium, $2,500 annual Deductible, 20% Co-insurance for in-network costs, 40% Co-insurance for out-of-network costs, an Out-of-pocket Maximum of $5,000 for in-network costs and an Out-of-pocket Maximum of $10,000 for out-of-network costs. Lastly, her plan doesn’t require any copays.

Since Jenny’s plan requires her to pay a significant amount more for out-of-network health care costs, she writes down a note to make sure she only visits doctors and hospitals that are in-network.

The Symptoms

About two months after enrolling in her health insurance plan, Jenny started having pains in her lower right abdomen along with symptoms of nausea and abdominal swelling.

As a result, she immediately made a same day appointment with her primary care physician. The physician asked Jenny a few questions, checked her vitals and ordered a lab test.

After 15 minutes of waiting, the physician came back and told Jenny he thought she might have Appendicitis, or inflammation of the appendix, but needed to order an ultrasound to be sure.

The Diagnosis

After viewing the ultrasound, the physician was certain now and diagnosed Jenny with Appendicitis, which required prompt surgery to remove her appendix (also known as an Appendectomy).

Jenny and her physician discussed options and made the decision to call her in-network hospital’s ER to put her on the list for an immediate appendectomy. Since Jenny was concerned about the costs of taking an ambulance and seemed okay to drive, the doctor agreed that she could drive herself to the ER.

So, Jenny drove to the ER, filled out many forms and waited to be seen by the ER surgeon. After one hour waiting, her name was finally called.

The Surgery

The doctors took her back, explained the surgery and answered Jenny’s questions. Then, they put her under anesthesia and performed the surgery.

Jenny’s appendectomy was a success with no complications!

The Recovery

After surgery, the doctors took her to the recovery room where she stayed to rest and recover overnight. The next morning, the doctors released her to go home where she would need to heal for a few weeks.

The Follow-Up

One week after her surgery, Jenny had to go back to her doctor for a follow-up visit so the doctor could make sure Jenny was healing according to plan. Her checkup went well and the doctor sent Jenny on her way to finish recovering!

The Medical Bills

Four weeks after her successful surgery, Jenny was feeling great. But, then she started receiving medical bills in the mail…

The first bill was a total of $300 from her primary care physician, which included the standard physician visit of $100 and the ultrasound cost of $200.

The second bill was a total of $15,000 from the hospital where she had her surgery, which included the appendectomy procedure cost, anesthesiologist cost and facility charges.

The third bill was a total of $75 from her follow-up visit with her surgeon.

The total medical bills for her appendectomy cost $15,375! And that’s the in-network cost.

The Math: How much does Jenny owe?

Now, let’s run the numbers to find out how much of the $15,375 Jenny owed and how much her insurance paid.

Since Jenny had not met any of her $2,500 deductible yet, she had to pay the $300 physician visit costs out-of-pocket, which counts towards her deductible. Now, she needs to pay $2,200 before her insurance will start paying 80% of her healthcare costs.

Next, Jenny paid the first $2,200 of her $15,000 surgery bill, which allowed her to hit her $2,500 deductible so insurance would kick in. Now, only $12,800 is owed on the surgery bill.

So far, Jenny has paid a total of $2,500 (her Deductible) towards her bills.

Since her out-of-pocket max is $5,000 and she’s hit her $2,500 deductible, Jenny only has to pay 20% of all remaining medical bills up to $12,500 [($5,000 OOPM minus $2,500 Deductible) divided by 20% Co-insurance]. Any future medical bills exceeding $12,500 will be covered 100% by her insurance company.

As a result, Jenny paid another $2,500 (20% of $12,500) towards the remaining $12,800 owed on the $15,000 surgery bill. And, the insurance company paid $10,000 (80% of $12,500) plus $300 ($12,800 minus $12,500) for a total amount of $10,300 towards the $15,000 surgery bill.

So far, Jenny has paid a total of $5,000 (her OOPM) for the first two medical bills.

Now that Jenny has hit her OOPM, the insurance company pays the full amount of the third bill of $75 and she doesn’t have to pay anything.

In total, Jenny had to pay $5,000 of the $15,375 medical bills while her insurance paid the remaining $10,375.

But, we’re not done yet…

Assuming Jenny never went to the doctor again that year, her total healthcare costs would be much higher after accounting for her health plan premiums.

As you recall, her monthly premium is $125/month for insurance coverage, which equates to $1,500 for the year.

As a result, Jenny spent a grand total of $6,500 on health care expenses that year ($1,500 premiums plus $5,000 out-of-pocket costs).

The Return on Investment (ROI)

Yes, $6,500 is a lot of money Jenny had to pay, but it definitely beats not having insurance and having to pay the full $15,375 on her own.

As such, I like to think of health insurance as an investment.

To calculate Jenny’s ROI on her health insurance coverage that year, we need to subtract her total cost paid from the total health care costs that year and divide that by her total cost paid [ROI = ($15,375 – $6,500) / $6,500].

For Jenny, her health insurance coverage resulted in a 1.37 to 1 ROI that year! This means that for every $1 she paid on health care expenses, she received an additional $1.37 to cover her costs.

This is exactly why we have health insurance in the U.S.

Health care costs are expensive and unpredictable. And, with our current health care system, we (the patients) bear the financial burden and risk of our health.

To mitigate our risks, we’re able to purchase health insurance to shift some of that financial risk and burden to health insurance companies. The health insurance companies are able to spread the risk across a pool of millions of other insured people and make a profit. They’re able to do this by charging premiums and since many people never hit their deductibles, thereby subsidizing those unlucky few who do get injured or sick.

That, my friends, is how health insurance works in the United States!

Do you need help choosing your health insurance plan?

Then continue on to Part 2 to learn how to choose a health insurance plan in 5 easy steps!

Want to be the first to know about my new posts? Sign-up for my newsletter below!